Update January 2 - When we first initiated coverage on Medical Property on November 12, 2023, we suspected the stock was ripe for a rebound. Our thesis was relatively straightforward: 1) the stock was under pressure from short-sellers, 2) it had traded down 50% (in November 2022), and 3) hospitals would continue to pay rent through economic volatility, supporting the underlying value of the real estate. Despite recognizing several issues (see below), we stated that we didn't think the stock was 'sick.'

Our diagnosis, however, was incorrect. The stock collapsed from a $12 price range in November 2022 to $5.06 as of January 2, 2023. What happened?

Interest rates increased significantly, forcing the company to put acquisitions on hold due to the sudden spike in rates. Additionally, several customers halted payments, and transactions with certain customers (e.g., Prospect) had to be restructured, resulting in significant demands on cash. Total revenues fell from $1.162 million for the 9 months ending September 30, 2022, to $994,182 for the same period in 2023. Net income for the 9 months ending September 30, 2023, plummeted to $107.5 million compared to $1.0 billion for the same period last year. Also, normalized funds from operations dropped from $1.38 to $1.22 for the comparable 9-month period.

Why sell the stock?

The answer is relatively straightforward. Unfortunately, the company's business model and structure are currently very complex. The restructuring of agreements for large properties introduces many unknowns and difficult-to-predict outcomes. If you're uncomfortable with the risk and the wait for a rebound, you might seriously consider selling

Last Update April 28, 2023 - On April 27, 2023, MPW held a conference call to report on its Q1 2023 performance, which ended on December 31, 2022. Most were expecting a disaster and a bunch of bad news. For us, we would use the French phrase "comme ci comme ca" which in English means "So-So."

Despite the poor stock performance, there were some positive trends. The company indicated that its U.S. hospital operator admissions has been steadily increasing over the past few months, with surgical volumes up year-over-year for the trailing 12 months Q4 2022 versus the trailing 12 months Q3 2022. The number of emergency room visits has also continued to increase since the beginning of 2022, with December seeing the highest ER volumes the portfolio had seen all year. Although we don't like to see people get sick, it is good for business.

There remain vocal shorts on the stock, which is clearly putting pressure on management, and we believe has scared off new and existing investors. These shorts have been questioning the business model, but from our perspective, the most important thing is liquidity.

MPW has also announced that the sale of its Australian hospital real estate investments would result in sufficient liquidity to repay the term loan used to fund the acquisition in 2019 providing significant relief to those concerned about the rapid rise in interest rates and related pressure on refinancing. The fact that it was able to sell its investment so soon, is evidence of the quality of its hospital real estate portfolio. Although we don't like to see the company, in effect, shrinking, it is more important to deal with investor perceptions.

Although the company announced some small acquisitions, they have now put larger acquisitions on hold due to the volatility of interest rates. With liquidity at approximately $1 billion at quarter-end, plus more than $900 million from announced sales, MPW is expected to be able to satisfy all of its roughly $1.4 billion in 2023 and 2024 debt maturities. This will give it breathing room as market conditions change and/or stabilize. It also announced its Q1 dividend.

There are still some issues related to Prospect, a troubled customer of MPW. Q1 revenue did not include rent or interest income from this customer which the company recognizes on a cash-received basis. Additionally, MPW agreed to invest $50 million into Prospect via a convertible loan. Although the shorts are viewing this as a "round-trip" transaction, the investment amount was actually more short-term and a reaction to the difficulties it had to obtain banking financing. It is also not really substantively different than a landlord investing in capital improvements up-front for a tenant. More importantly, MPW indicated that Prospect had received a binding commitment from several third parties for additional financing. Once this commitment closes, we should expect to see some pressure of the stock.

The past 3-4 month stock price decline, we believe was largely due to vocal shorts who were taking advantage of market disruptions related to the banking industry in the fourth quarter, which impacted global credit and blew up a prior financing deal that Prospect had. We believe the financing market will ultimately stabilize and are confident in MPWs long-term sustainability. With respect to the vocal shorts, MPW filed a lawsuit against some of them, showing confidence in its numbers and a willingness to stand behind its representations to the market.

Although there have been some bumps in the road, sophisticated investors should get comfortable with MPW based on the long-term sustainability of its model, including receipt of annually inflation-adjusted rents from local hospital operations. As inflation occurs, the benefits will flow through the bottom-line and as dividends to shareholders

____________

Prior Publication - January 14, 2023

January 14, 2023 - New York - The New Year has started out healthy for those that bought stock. Medical Property Trust (MPW) was trading at around $11.00 per share when we suggested that short sellers in the stock were exaggerating concerns about the company. The stock at the close of business today is $12.09 which translates into an unrealized gain of approximately 10% for those who bought the stock. The current yield on the stock is still over 10%.

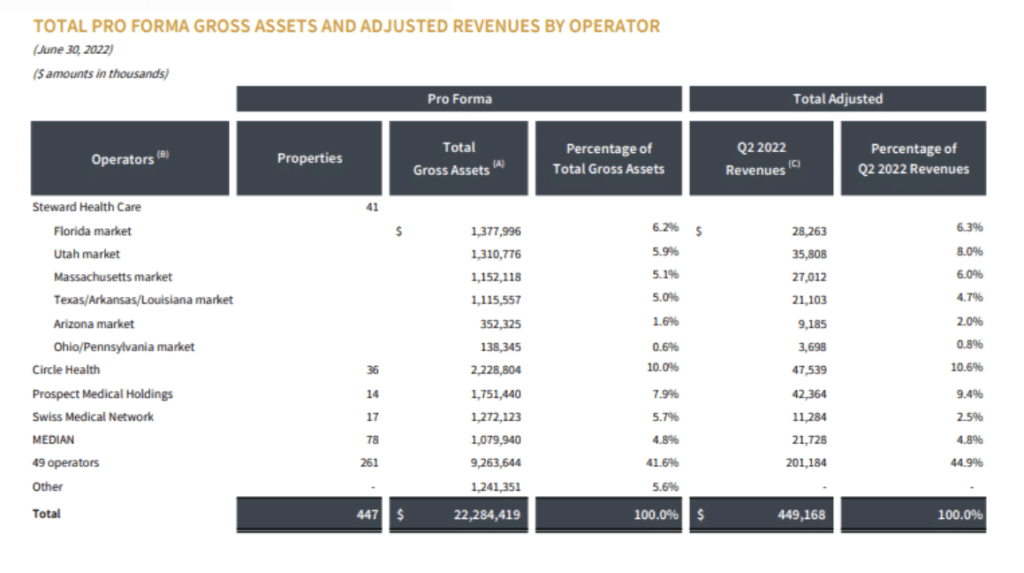

In late December, MPW's largest individual hospital tenant known as Steward Health Care (see chart below) was able to extend its credit deal with lenders through December 2023. There were concerns that Steward would be unable to do so because it had not yet published annual financial statements. Moreover, Steward was the subject of a negative article published by the Boston Globe.

Obviously, if the banks were willing to extend credit for a year --- they would have had access to Stewards' internal financials which was good enough for them. Issuing audited financial statements is something we would like to see, and we'll keep our eye out for it. But in the meantime, we stand behind our positive position on the stock.

____________

Original Publication - November 12, 2022

MPW has been under fire by short sellers. Is it sick? We don't think so.

It is critical for an investor in hospital real estate (MPW is a basically a hospital REIT) to understand the value that a specific facility has to the healthcare needs of the community it serves. Said differently, if people need medical services, they usually don't shop but go to the local health care facility regardless of who runs it. At the same time, it doesn't mean you should not invest in a hospital REIT just because the goals and periodic performance of one particular operator are not met in a certain location. For us, MPW is about location and the value of real estate that is zone and built up for medical uses. If you buy MPW low and sell high, we believe a real estate investor can enjoy attractive, well underwritten returns.

MPW has made some mistakes. It has had poor communication related to a hospital operator (a customer) who filed Chapter 11. They have some other troubled customers as well. MPW has had some Board turnover. MPW has even had legal issues (that were fully resolved 100% in the company's favor). And just because short sellers have started a campaign against the management team accusing them of malfeasance, it does not at all mean that when a CEO invests in a partnership that does business with a customer or company he runs, it always should make investors run-away.

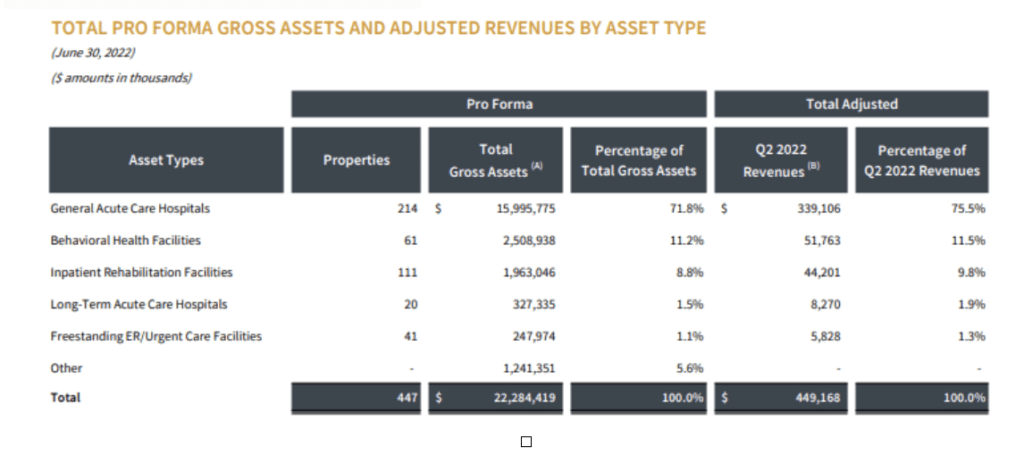

Let us stick with facts. MPW has a tremendous history of growth and generating cash flows. It has built up a somewhat diversified global platform with 438 properties in the U.S, Australia, Germany and the UK, among other countries.

They do have a large customer in Steward Health Care - but that customer has multiple markets.

Steward Health Care is undergoing some financial stress as it recovers from various issues including the strain on expenses due to the Coronavirus.

Here is our view:

MPT currently has a $2 billion revolving credit facility with extension options to June 2026. It has various short-term debt due ---400 million pound sterling in December 2023 and then in 2024 - a $750 million term loan due (that was used to acquire a portfolio in Australia). It seems to us that refinancing hospital secured debt should not be a problem. Albeit -there maybe some higher interest rates as compared to historical levels. Debt to leverage ratio is higher ---somewhere around 7 to 9x EBITDA depending on how you calculate. We think about leverage here like buying a house. If an individual home owner purchases a single family home and puts 20% down, 80% of it is funded by debt. On a single property, that is high - but that is where diversification comes into play.

Although Steward Capital is a large customer - roughly 25% of total assets - those assets are held in multiple markets - the largest of which is in Florida at 6.5%.

MPT continues to generate cash. Cash funds from operations (FFO) for this year is expected to be around $1.80. With the stock around $11 (at the time we write this research brief) that is a double-digit or 15% FFO ratio.

But clearly, MPT is not in a growth mode now due to high interest rates.

We believe it has a long-standing, consistent and successful business model has always been to invest in hospital real estate that regardless of the operator is underwritten to generate sustainable, long-term cash rental revenue. The key investment criteria for this success is acquisition of real estate that is critical to the delivery of hospital services in any particular community. We believe it is a mistake for real estate investors or analysts to assess hospital value based primarily on periodically volatile operating results instead of the important characteristics of the underlying real estate.

Hospitals will pay rent through economic volatility, Obamacare, the Affordable Care Act, and continuing disruptions, uncertainties and the aftereffects, three years of an unprecedented global pandemic that included virtually closing many hospitals for months. With higher interest rates on the horizon, new investments will be scarce - and the dividend yield payout may have to be reduced.

Are there some issues? Sure. However, with the stock down almost 50% in the past year and trading down 17% over the past 5 years, we believe such risk is priced in.

About Us

Founded in 1998, The Independent Adviser Corporation has assisted thousands of individuals, families, and businesses. We are 100% independent and 100% objective and offer free private consultations. Our company publishes free investment research and educational materials, and when financial or legal advice is needed, we connect individuals with a network of FEE-ONLY professionals. What are you waiting for? For more information, become a member or to schedule a free consultation with a Fee-Only adviser in your area, please visit our website at TheAdviser.com or 1800ADVISER.COM.